Video Gallery

Why Can’t You Keep Property Tax Outsourcing in the US?

PropTax Minute

Welcome to Advantax. I’m Regina Waldroup with your PropTax Minute.

Outsourcing became a part of the business lexicon in the 1980s, and is simply subcontracting a process to a third party. When property taxes are outsourced, it allows a company to focus on its core competencies. Unfortunately, there are some misconceptions about outsourcing property taxes.

One misconception is a loss of jobs, especially American jobs. Property tax returns can be processed in a cost effective fashion without transferring them overseas. If this is important to you, look for firms who process property tax returns in the United States. Ask who will be processing your returns and where.

Another misconception of outsourcing is a loss of control. With today’s technology, companies can successfully transition their work, but not lose control. The relationship between the company outsourcing and the outsource provider should be like “the office next door”. Ask about transparency and what it will look like with an outsource provider.

For more information about outsourcing, visit us at Advantax.com.

Thanks for watching PropTax Minute.

Property Tax on Sheep and Goats of Breeding Age

PropTax Minute

Welcome to Advantax.

I’m Owen Jensen with your PropTax Minute.

Just when you think you’ve heard of every property tax possible., this one is one of the more interesting ones, to say the least.

In West Virginia, when filing a commercial business property return, there’s a section for “number of sheep and goats of breeding age.”

The instructions ask the preparer to fill in the number of each and then remit $1 for each head with the completed form.

According to a 2001 study, the breeding ewe and lamb population in West Virginia was about 28,000. As a result, the maximum collectable property tax would be $28,000, which some might argue hardly pays for an auditor to drive around the state to visit all the sheep farmers.

And it appears that tax on sheep is not a new thing. In 1549, England imposed a tax on sheep with different rates for different breeds. It was the shortest-lived tax in English history.

In 2003, New Zealand took a different approach… they proposed a tax, not on the sheep themselves, but on the flatulence emitted by sheep, cattle and deer. You can imagine how difficult it would be to manage that tax!

Just some property tax implications to keep in mind, next time you consider raising sheep and goats.

For more property tax news, check out the PropTax Minute at advantax.com

Thanks for watching.

How Do I Quantify Obsolescence?

PropTax Tutorials

Welcome to the final in our series of three PropTax Tutorials dedicated to the topic of obsolescence. In our earlier PropTax Tutorials, we introduced the concepts of functional and external obsolescence. Functional obsolescence – being defined as the loss in value due to the inability to perform adequately, or in the manner that the property did when it was created. The issue is internal to the property. And, external obsolescence being defined as the loss in value due to impairment in utility caused by factors external to the property. We talked about ways to identify obsolescence. Now that you’ve identified that your property may be experiencing obsolescence, the question becomes, “how do I quantify obsolescence?”

I’m glad you asked. It’s one thing to know you’ve got it and quite another to quantify it. There are two primary ways to quantify obsolescence – calculating the excess operating costs and calculating the excess capital costs caused by the obsolescence. In other words, obsolescence causes more expense in the operation of the property and more expense in the capital cost structure of the property.

Let’s start with excess operating costs. Obsolescence can be quantified by calculating the difference in cost to operate your property compared to a modern version of your property. It is basically quantifying the value in dollars lost by continuing to run obsolete property versus upgrading it. The costs we’re talking about here are gas, electricity, labor. Any operating cost.

A common example is that old washer and dryer that may still be hanging around your house. Modern washers and dryers have become much more cost effective to operate. They take less electricity and therefore cost less money to operate. If we quantify the difference in annual expense between the old and the modern units, we can quantify obsolescence. Once the excess annual cost is identified, you must take the present value of future excess costs to calculate total obsolescence. In other words, what is it going to cost over the future years to continue operating this property but calculated in today’s dollar. That’s essentially what an investor valuing your property would deduct from the value. So which equipment line or buildings is costing you more to operate than what a modern version would cost?

When it comes to excess capital costs, things get a bit more complicated. There are two ways to quantify excess capital costs – calculating the excess costs to build your property compared to today’s costs for a modern property. This is called reproduction versus replacement cost. The second is calculating the excess costs due to reduced utilization of your property. This is called cost to capacity.

Let’s use the example of the brick phone from our earlier PropTax Tutorial, to explain the reproduction versus replacement cost calculation. The brick phone probably cost around $2,000 back in the day, and would cost even more to reproduce it exactly as it is today. Current reproduction cost would be taking an exact replica in today’s dollars, which would result in something higher than $2,000.

But we all know that brick phone can be replaced by a smart phone for about $100. The replacement cost, not reproduction cost, for the brick phone is a $100 smart phone. You can calculate obsolescence by taking the difference between reproduction cost new, $2000+, and replacement cost new, $100, which comes to $1900. Another example of this can be seen with multi-story manufacturing buildings. Not only is it more efficient to build a one story facility, it generally costs less to build. By looking at the difference between reproduction cost new and replacement cost new, we can calculate excess capital costs.

Cost to capacity, the second way to calculate excess capital costs, measures the loss in value due to reduced utilization of an asset. The reduced utilization is typically tied to obsolescence. For example, let’s say you have a 10,000 gallon tank that was built to house a very special and exotic water. Only this kind of tank can be used for this type of water. Everyone loves the water and the tank is used to capacity, 10,000 gallons. Certain people get sick, not everyone, but people with certain conditions. The government restricts the use of your special water. There is reduced demand and the max the tank can be used going forward is 6,000 gallons. Basically you could run the operation with a 6,000 gallon version of the special tank but you have a 10,000 gallon tank. Cost to capacity is calculating the excess cost for the 40% of the tank that will not be used going forward.

You could argue that the tank deserves a 40% reduction in assessed value but a more accurate calculation would take that 40% multiplied by a scale factor to come up with something less than 40%. The scale factors, typically between .6 and .95, account for the reality that the cost to increase capacity is rarely a one for one relationship. Typically scale factors come from an engineering table.

In the past few minutes, we’ve covered quantifying obsolescence. There are whole courses devoted to the discussion of obsolescence. Hopefully, this PropTax Tutorial has peaked your curiosity and challenged you to begin the journey of looking for and quantifying obsolescence in the equipment and real estate owned by your company.

If you have questions regarding your property taxes please contact us at advantax.com. Thanks for watching PropTax Tutorials, one of the many ways Advantax is demystifying property taxes.

A Federal Property Tax?!?

PropTax Minute

Welcome to Advantax. I’m Owen Jensen with your PropTax Minute.

With the national debt soaring into the trillions, and lawmakers constantly searching for new ways to haul in revenue, try this one for size: a federal property tax? To our knowledge, no one’s proposing it right now, but don’t be surprised if the idea comes up. It’s got history on its side.

In 1798 the U.S. had an “undeclared war with France” after they captured hundreds of us merchant vessels. In an effort to fund the “war”, congress passed a national property tax. Property was divided into three categories: houses over $100, land and houses under $100, and slaves. Assessors in each of the 16 states were authorized to carry out the property tax. Values were established and taxes were collected.

Then fast forward to 1943 when three economists, commissioned by the government, wrote a proposal to modernize property taxation. They recommended dozens of reforms to centralize and standardize property assessment at the federal level.

World War II had changed people’s opinions on taxation. People, in general, were motivated to contribute to the war effort at all levels. In fact, the revenue act of 1942 forced most workers to pay income tax for the first time and still opinion polls consistently showed 85-90% of people thought the new taxes were fair. However property taxes weren’t quite as popular, though, because they didn’t go directly to the war effort. This, coupled with overwhelming disagreements in congress, killed the idea of a federal property tax.

For more property tax news, check out the PropTax Minute at Advantax.com

Thanks for watching

Tax Like an Egyptian

PropTax Minute

Ever look at your property tax bill and wonder, “Who created this tax? Whose idea was it to tax property anyway?” The answer: ancient Egypt.

Starting in 3,500 B.C., Egypt created one of the first pictures of how this property tax thing should work. Farmers and land holders in Egypt paid property taxes equal to about ten percent of the land production. If the person who was being taxed could not or would not pay, he was taken to the courts for justice.

In many of the ancient Egyptian tombs, wall paintings depict village elders being punished for trying to ignore or evade property taxes. Ancient Egypt’s system and need for property taxes is not so different from what we see in our system today.

By the way, as a child you may not have dreamed of someday becoming a property tax collector, but that’s because you weren’t born in ancient Egypt. In ancient Egypt, only about one in a hundred citizens were literate. Among those were the tax collectors of the day, also known as scribes.

And there you have it. Next time you get that bill, you can blame it on ancient Egypt.

For more property tax news, check out the PropTax Minute at advantax.com. Thanks for watching.

How Do I Identify Obsolescence?

PropTax Tutorials

In our last tutorial, “What’s Obsolescence?”, we introduced the concepts of functional and external obsolescence. Functional obsolescence, being defined as the loss in value due to the inability to perform adequately, or in the manner that the property did when it was created. The issue is internal to the property. And external obsolescence being defined as the loss in value due to impairment in utility caused by factors external to the property. The responsibility of identifying, quantifying and reporting obsolescence falls on the taxpayer. If there is going to be a reduction in your property tax assessment and the subsequent property tax bill due to obsolescence, obsolescence must first be identified. So how does one identify obsolescence?

In order to identify obsolescence, we need to identify the causes of obsolescence. Causes of functional obsolescence generally revolve around a change in technology or a design change. Let’s take a manufacturer for example. When a production plant is built it is usually built with the latest and greatest design. Over time new and better ways to design are introduced, making newer plants faster and more efficient. The original plant experiences functional obsolescence. It has become inadequate. This inadequacy may be throughout the plant or only within sections of it.

The reverse of inadequacy can also occur. It’s called “super adequacy”. Super adequacy reflects building more design into a property than the market really cares about. We see this sometimes with corporate headquarters built to make a statement. It’s important to point out that inadequacy and super adequacy are measured by the marketplace, through the eyes of a potential purchaser of the property. All things considered equal, a purchaser would pay less for a property that exhibits obsolescence when compared to one that does not. Why pay as much for a property exhibiting inadequacy in technology or design? Likewise, a purchaser will not pay as much for a super adequate facility. Why buy the Taj Mahal when a simple cemetery plot will do?

Causes of external obsolescence include issues beyond the control of the taxpayer, such as government restrictions. The value of asbestos making plants and equipment dropped dramatically in 1978 when the U.S. government banned asbestos.

An unfavorable location is another cause of external obsolescence. A company builds a beautiful office in a neighborhood. Over time the neighborhood decline significantly to the point that it is undesirable to have an office there. While the office may still be beautiful, an investor will consider it less valuable because of the neighborhood.

Product supply and demand is another cause of external obsolescence. A sharp decline in demand for a product may cause the equipment and facilities producing that product to drop in value. For example, we worked with a chemical manufacturer who was experiencing supply and demand issues. Their Chinese competitors were selling the same product in the U.S. at a price lower than the manufacturer’s cost to product the same product. Their production facility, which cost millions to build just a few years earlier, had greatly diminished in value. What investor wants to pay for a plant that will cost him money to operate? That’s external obsolescence.

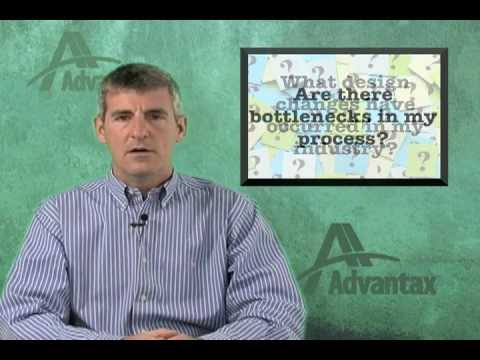

Functional and external obsolescence can occur in almost any type of equipment or building. Identifying obsolescence starts by asking questions. Questions like,

• Has technology negatively impacted my plant or equipment?

• What design changes have occurred in my industry?

• Are there bottle-necks in my process, causing it to be in adequate?

• Do I have inactive equipment?

• Why is it inactive?

• Did we overbuild?

• Is our operation profitable? If not, why?

By looking at the causes you’ll be able to identify obsolescence, which is the first step. Quantifying obsolescence is another matter – one that will be covered in our next tutorial.

If you have questions regarding your property taxes please contact us at advantax.com. Thanks for watching PropTax Tutorials, one of the many ways Advantax is demystifying property taxes.

Property Tax Responsibility…On Both Sides

PropTax Minute

Welcome to Advantax. I’m Owen Jensen with your PropTax Minute.

Is your company considering pursuing legitimate property tax refunds? Some simply don’t, because they fear community backlash, including from school districts who depend on that money. After all, no company or CEO wants to be accused of “taking money from the children.”

But the real question may be – where does fiscal responsibility on the part of school districts (or any government entity receiving property tax funds) come into play? And why are the politics of “taking money from the children” used against corporations who do pay their fair share and sometimes even more than their fair share.

In one example, a company had been over assessed for years and finally negotiated a settlement with a school jurisdiction who we’re not going to identify here.

The appeals and subsequent settlement included refunds of over $1 million. No chump change by any means.

In a last ditch effort, the school superintendent strongly urged said company to just forget the money, and let the school district keep it.

But the company had done its prior research and learned the school district was actually spending on its students thousands of dollars more than the national average.

Confronted with those facts, the settlement was quickly accepted.

This case was not about “taking money from the children”. In reality it had more to do with using common sense in how the funds are spent.

If your company is struggling with excessive property taxes, while at the same time wanting to be a good corporate citizen, we can help. Contact us at advantax.com

Thanks for watching.

What’s Obsolescence?

PropTax Tutorials

Obsolescence is a term thrown around in the property tax industry. But what is obsolescence? Obsolescence is the state of being which occurs when an object, service or practice is no longer wanted even though it may still be in good working order. The horse drawn buggy is an example of equipment that may suffer from obsolescence. While it may be still in good working order, it is generally no longer wanted as a form of transportation. The typewriter is another example. While a typewriter may be in pristine shape, it is less desirable due to the advent of personal computers, tablets and smart phones.

Why is this important to property taxes? Property taxes are based on the value of equipment and real estate. Obsolescence can significantly affect value and is something to consider when reviewing your property tax assessment. It isn’t something the assessor’s office is likely to contemplate unless you bring it to their attention.

There are two types of obsolescence: functional and external. Functional obsolescence is the loss in value due to the inability to perform adequately, or in the manner that the property did when it was created. External obsolescence is the loss in value due to impairment in utility caused by factors external to the asset. Another way to look at this is functional obsolescence is caused by internal forces and external obsolescence is caused by external forces.

Let me give you some examples of functional obsolescence in the real world. Multi-story processing plants are an example of real estate that suffers from functional obsolescence. Why does it experience functional obsolescence? Many years ago processing facilities were commonly built as multi-story facilities, using gravity to move product down through the floors. At the time, the multi-story design was considered very useful but over time there have been significant design changes and production improvements. Modern plants are typically built in a one story layout for process flow. An investor would likely pay less for a multi-story production facility than a one-story facility, all things considered. The multi-story facility suffers from functional obsolescence.

The brick phone is an example of a piece of equipment that suffers from functional obsolescence. Do you remember the brick phone? It was huge and very cool in its day. You could call your friends from it for $3 per minute. We all know that technological improvements have allowed new smart phones to function in a much more efficient and cheaper fashion. The brick phone is bulky and last i heard difficult to load apps on. It suffers from functional obsolescence. By the way, does anyone still have a brick phone?

Examples of external obsolescence are similar, except, as the name suggests, external obsolescence is caused by factors external to the facility or equipment. Asbestos plants are a good example of external obsolescence. Prior to 1978 asbestos was used in all kinds of building construction. In 1978 it was deemed to cause cancer and banned in the U.S. How rapidly do you think the value of an asbestos producing plant fell on news of the ban? That is an example of external obsolescence.

Another example of external obsolescence, on a smaller scale, much smaller, is the beanie baby. Do you remember the craze for beanie babies? When they first came out beanie babies could be purchased for under $5 but then something really interesting happened. Due to high demand and low supply, the value soared for certain beanie babies. Princess Di and peanut, the elephant became extremely rare and people paid hundreds of dollars for them. In fact, I knew people who were investing in them. Then what happened. Demand fell and supply soared and they were all worth about $5 again. An example of external obsolescence.The concept of obsolescence is important in determining value for property tax purposes. If your equipment or real estate is suffering from obsolescence, it should probably result in a lower value and subsequently lower property tax bill. The steps to accomplish this are identifying, quantifying and reporting obsolescence. We’ll cover these in future Proptax Tutorials.

If you have questions regarding your property taxes please contact us at advantax.com. Thanks for watching PropTax Tutorials, one of the many ways Advantax is demystifying property taxes.

Big Ass Fan

PropTax Minute

Welcome to Advantax. I’m Owen Jensen with your PropTax Minute.

Is an asset personal property or real property? Sometimes it’s quite confusing. For example, how should fans be treated? Personal property? Real property?

There’s a company called Big Ass Fans. We’re not making this up. They provide industrial, commercial and residential fans. And as you can imagine, as the name implies, they are really big fans.When it comes to property taxes: should that big ass fan be included on your personal property return?

“Do best practices in property tax compliance require reporting of such items as personal property?” The underlying issue is whether the fans are personal property or real property in the first place.

Real property assets are usually not reported on the personal property return (with a few exceptions) so as not to double count them as both real and personal property. As a general rule: if the intended use of your fan is to provide cooling to the facility and the people working in it, it’s probably real property. If its intended use is to cool down equipment, it’s probably personal property.

Hopefully, that should help cool things down a bit.

If you need assistance determining if the assets you’re reporting are personal or real property, contact us at advantax.com

Thanks for watching.